Europe’s $690 Billion Bet: Why the Physics Lab is Replacing the Code Editor in 2026

▼ Summary

– The European deep tech sector is thriving, reaching a record $690 billion in total enterprise value and attracting 32% of all European VC investment in 2025.

– Deep tech funding has shown remarkable resilience, remaining near its historical high while conventional tech investment has fallen sharply from its peak.

– Investment is concentrated in specific technologies, led by Novel AI and the Future of Compute segment, which saw 115% year-over-year growth.

– A significant structural challenge is a late-stage funding gap, with 70% of growth capital coming from non-European investors, creating a dependency risk.

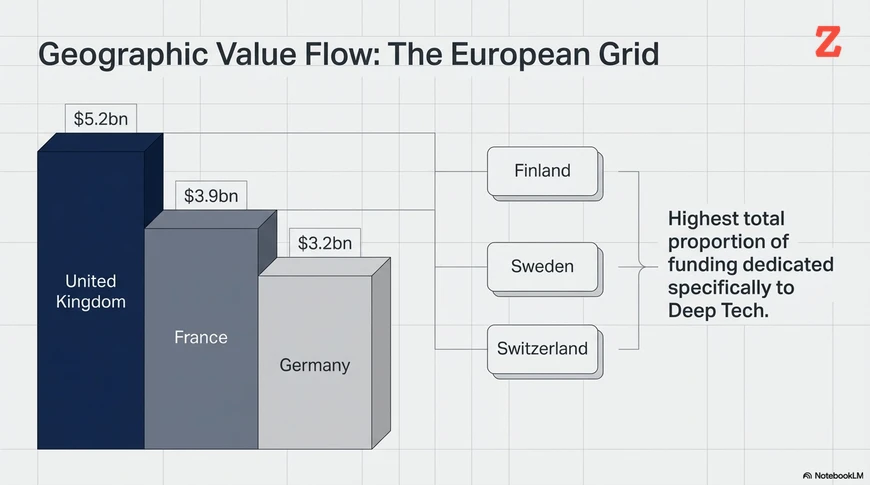

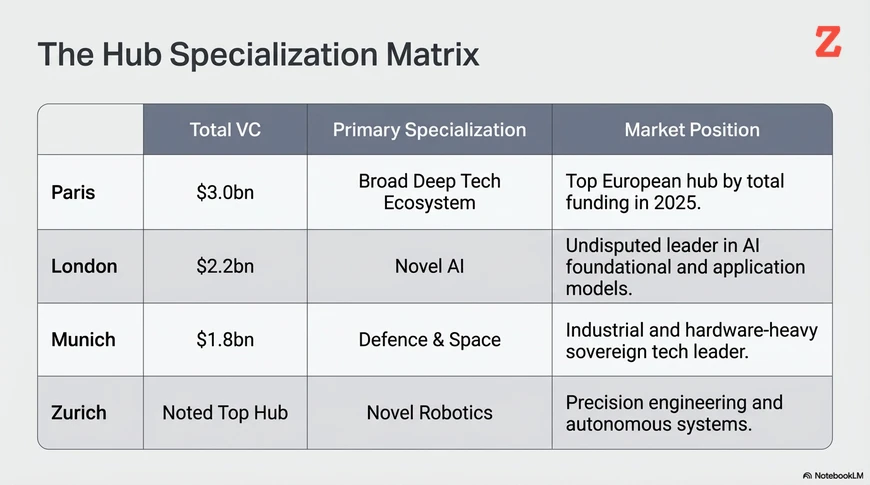

– The UK, France, and Germany are the top funding countries, with Paris emerging as the leading European city for deep tech VC investment in 2025.

The Shift from Bits to Atoms

For nearly two decades, the venture capital playbook was written in “bits”: scalable, pure-software plays that could be built in a garage and deployed globally with near-zero marginal cost. But by 2026, the game has fundamentally changed. As generative AI commoditizes code and erodes the traditional moats of “shallow tech,” the hunt for true defensibility has shifted from the screen to the lab. The race to the bottom in software has led us to the new high ground: “atoms.”

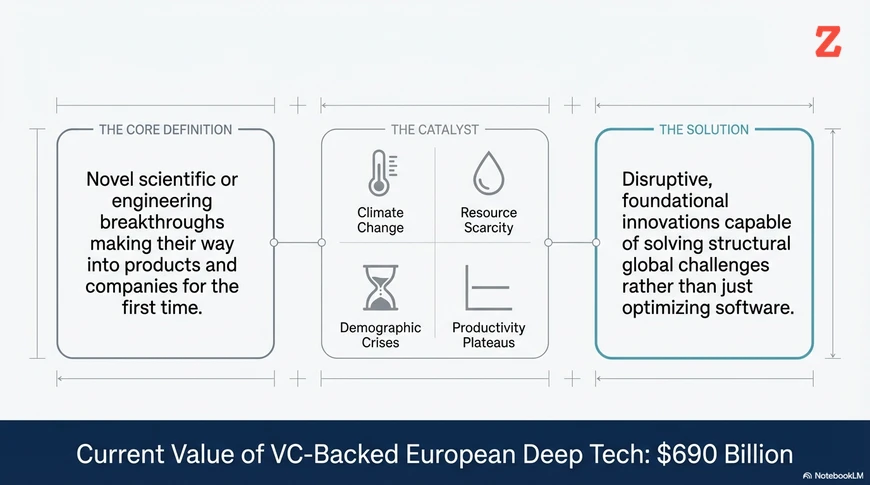

Deep Tech, defined as the “first-time productization” of novel scientific or engineering breakthroughs, is no longer a peripheral interest for the curious. It has become a strategic necessity. In a year where 2025 was recorded as the third hottest on record, and as Europe faces a looming dependency ratio crisis (where fewer workers must support a rapidly aging 65+ population), the demand for “hard” solutions has never been more urgent.

Whether it is decarbonizing energy systems through long-duration storage or addressing resource scarcity as the demand for lithium and cobalt skyrockets, 2026 represents a pivotal year. Europe is no longer just iterating on digital applications; it is leveraging fundamental science to solve the world’s most pressing existential threats.

Resilience in the Storm: Deep Tech vs. “Regular” Tech

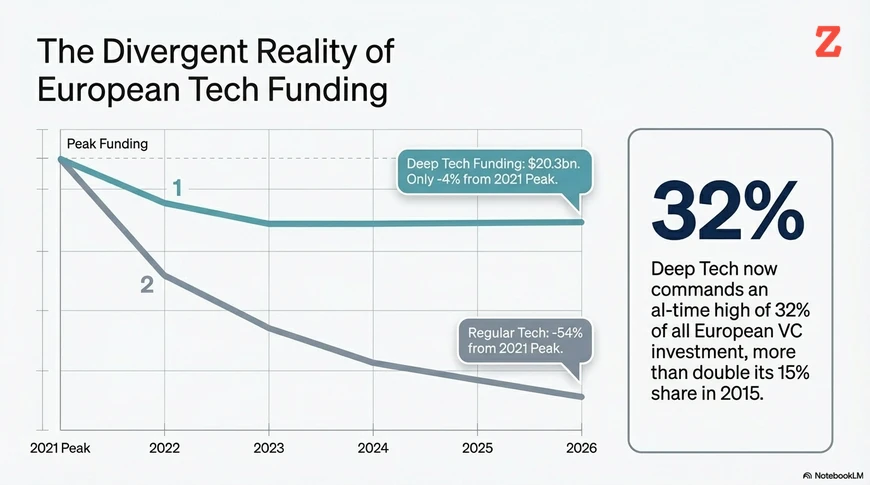

While the broader technology market has spent the last few years recalibrating, Deep Tech has emerged as the “adult in the room.” The numbers tell a story of remarkable structural resilience. While “Regular Tech” has suffered a staggering 54% decline from its 2021 funding peak, Deep Tech has remained nearly steadfast, experiencing a mere 4% dip.

In 2025, investment in the sector rose to $20.3 billion, now commanding a record 32% of all European VC investment, more than double its 15% share a decade ago. From a strategic perspective, this isn’t just about stability; it’s about performance. Data suggests that Deep Tech portfolios are beginning to outperform conventional tech, as investors realize that companies solving fundamental problems like resource extractability and energy sovereignty are less susceptible to the fickle cycles of consumer discretionary spending.

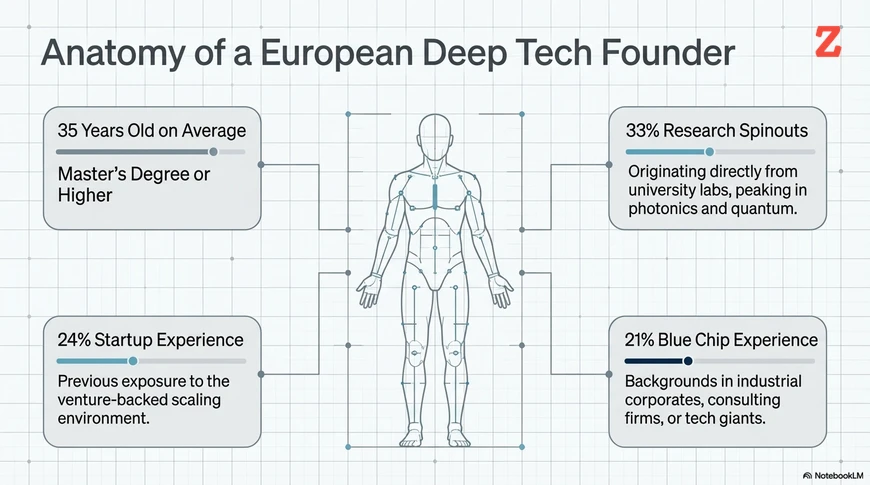

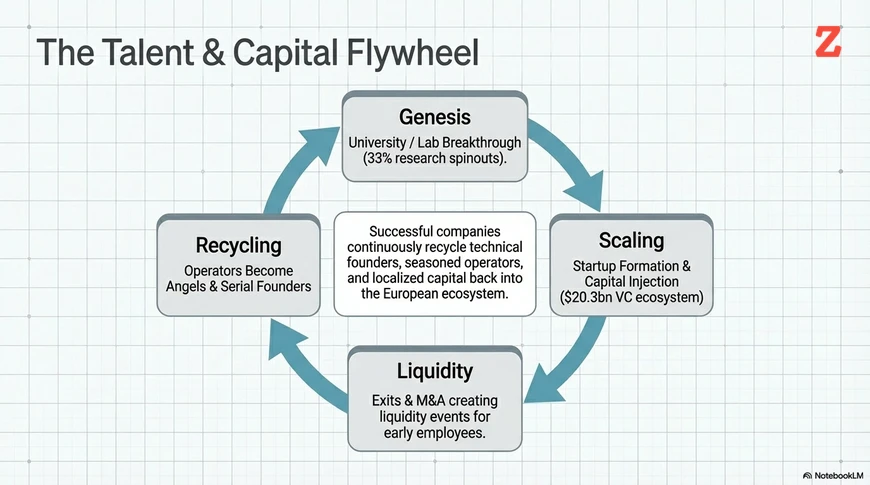

The Talent Flywheel: Europe’s Unfair Advantage

Europe’s most potent weapon in this new era is its concentrated pool of raw human capital. The continent produces 1.5 million STEM graduates annually, more than double the output of the United States. It also hosts 30% of the world’s top Deep Tech universities, with institutions like Oxford, ETH Zurich, and the Technical University of Munich (TUM) leading the charge in physical sciences and engineering.

We are now witnessing the first rotations of a “talent flywheel,” where successful operators from the first wave of European unicorns are recycling capital and expertise into the next generation of labs. Paul Murphy, Partner at Lightspeed Venture Partners, captures the shift:

“The quality of European talent, both technical and commercial, is world-class, full stop. At Lightspeed we back companies globally, and the best founders we meet in London, Paris, or Munich are operating at exactly the same level as their counterparts in San Francisco or New York. The honest constraint isn’t quality, it’s quantity… That flywheel is just getting started, and it’s one of the most exciting structural shifts happening in European tech right now.”

However, a friction remains: the “Researcher to Founder” pipeline. While Europe owns the science, the transition from the laboratory to the boardroom remains a hurdle that the ecosystem must clear to truly scale.

The Sovereignty Surge: Defence and Space Take Center Stage

Geopolitical instability has transformed “sovereignty” from a political buzzword into a massive investment thesis. The demand for local supply chains and sovereign technology has sparked a surge in Defence and Space funding. Defence tech saw a 125% explosion in funding to $1.8 billion, led by heavyweights like Helsing, which recently secured a €600 million round, and Quantum Systems (€340 million).

Space Tech followed suit with a 22% rise to $1.3 billion, anchored by the progress of Isar Aerospace (€150 million) and EnduroSat (€153 million). But the surge isn’t limited to security:

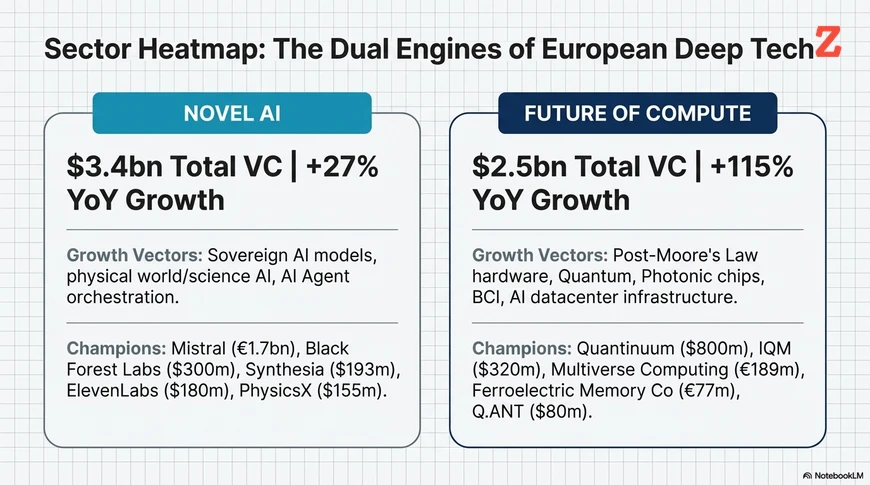

- Future of Compute: $2.5 billion (+115%), with Quantinuum ($800 million) and Mistral (€1.7 billion) redefining the hardware-software stack.

- Computational Biology & Chemistry: $1.1 billion (+88%), as AI-driven drug discovery moves ‘in silico’.

- Novel Robotics: $468 million (+64%), with Zurich emerging as a global hub for cognitive and autonomous systems.

The 2025 Deep Tech Sector Breakdown

| Technology Segment | 2025 VC Funding | YoY Growth | Key Growth Drivers & Notable Movements |

| Novel AI | $3.4bn | +27% | Foundational models (e.g., Mistral €1.7bn) and AI for vision/voice (e.g., Synthesia $193m). The focus is shifting to sovereign models and robust agentic workflows. |

| Future of Compute | $2.5bn | +115% | Quantum computing hardware (e.g., Quantinuum $800m), novel memory, and photonic chips tailored for post-Moore’s Law infrastructure. |

| Defence | $1.8bn | +125% | Driven by geopolitical conflicts, capital is pouring into sovereign solutions leveraging AI and drones, highlighted by Helsing’s €600m raise. |

| Space Tech | $1.3bn | +22% | Expansion in Earth observation, small satellite manufacturing, and launch vehicles to enable European sovereign launch capacity. |

| CompBio & Chemistry | $1.1bn | +88% | Heavy investments in AI-driven drug and material discovery moving ‘in silico’, led by Isomorphic Labs ($600m). |

| Novel Robotics | $468m | +64% | Cognitive and autonomous systems, with Zurich rapidly emerging as a global hub for the talent and engineering required. |

The Speed of Innovation: From Decades to Months

The timeline for a breakthrough to reach the masses is shrinking at a rate that traditional industry can barely track. The “Deep Tech Journey” is moving from “Technological Uncertainty” to “Mass Adoption” with unprecedented velocity.

- Personal Computer: 36 years to reach 1 billion users.

- Internet: 25 years to reach 1 billion users.

- Generative AI: 3 months to reach 1 billion users.

While LLMs have successfully transitioned from the lab to mainstream adoption, the next wave, Quantum Computing, Nuclear Fusion, and Humanoids, is currently navigating the “Will it work?” phase. For the strategic analyst, the primary risk has shifted from “Market Risk” (is there demand?) to “Development Risk” (can we make the science work?). If a technology like Fusion (led by Proxima Fusion’s €145 million effort) works, the demand is essentially infinite.

The “Physical World” Moat: Defensibility in the Age of AI

In an age where generative AI can replicate “shallow tech” interfaces in a weekend, Deep Tech offers the last bastion of true defensibility. Unlike software, which faces high competition risk, Deep Tech faces “Development Risk.” The capital in this sector is spent building hardware, novel materials, and intellectual property that is anchored in the physical world.

This “physical world moat” means that once a company proves its technology, it faces almost no competition for years. While the CapEx is higher and the timelines longer, the revenue acceleration at maturity is often steeper. You cannot “prompt engineer” a satellite launch vehicle or a photonic chip; these require years of patient engineering that simply cannot be recreated overnight by a model.

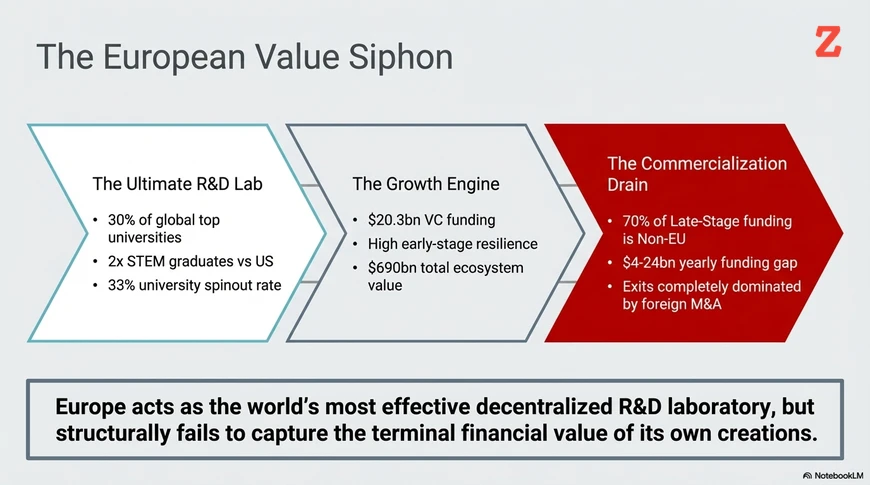

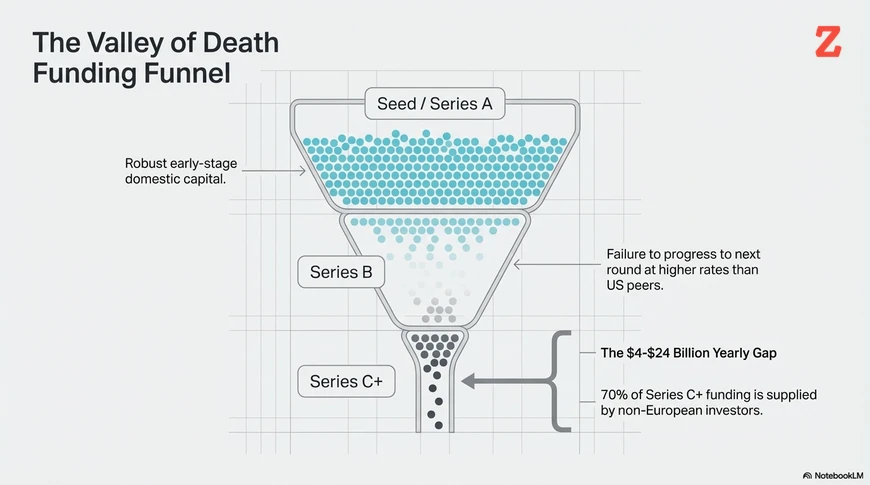

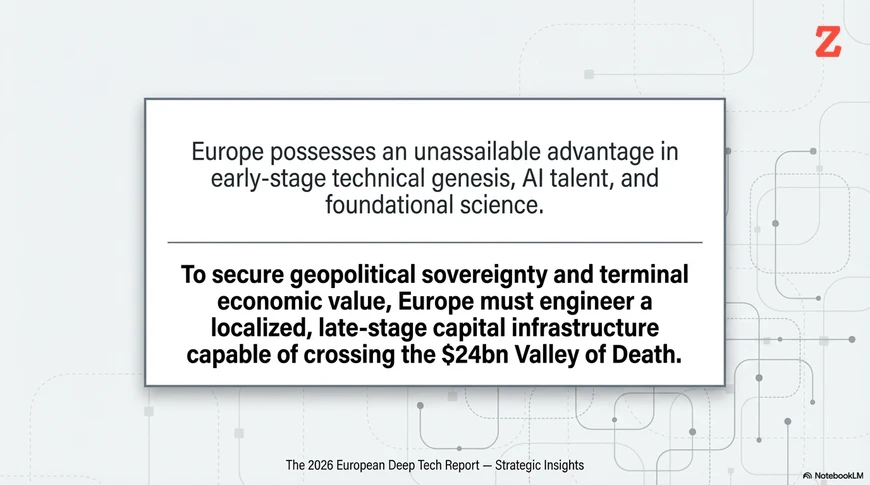

The $24 Billion Warning: The Late-Stage Funding Gap

Despite the abundance of talent and early-stage momentum, Europe faces a structural crisis: the growth-stage funding gap. While Series A is well-covered, there is an annual shortfall of $4 billion to $24 billion for late-stage scaling.

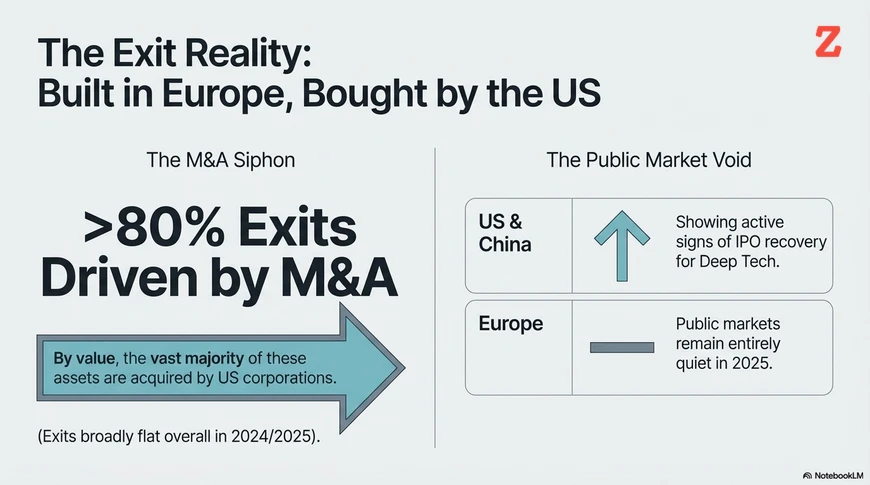

The data is sobering: 70% of late-stage funding for European Deep Tech now comes from non-European investors. This creates a dangerous drift in the “geographic centre of mass.” When US or Asian investors dominate the cap table of a European champion, the intellectual property, leadership, and eventually the tax base, tend to follow the money. Without a shift in local risk appetite, Europe risks becoming a high-end research lab for the rest of the world’s corporate giants.

Conclusion: A Provocative Look Ahead

The European Deep Tech ecosystem is currently a $690 billion opportunity, fueled by world-leading research and a new generation of ambitious founders. The “raw ingredients” are undeniable, yet the path to global leadership is blocked by four core challenges: the late-stage funding gap, regulatory fragmentation, the researcher-to-founder friction, and a persistent lack of risk appetite among European corporates.

The science is here. The talent is here. The geopolitical necessity is here. But as we look toward 2027, one question looms over the continent: Can Europe find the courage to fund its own future, or will it continue to watch its most vital innovations be harvested by the very competitors it seeks to lead? The next 24 months will decide if Europe is a sovereign tech power or merely a laboratory for the highest bidder.